Abbott Laboratories: Volatility Creates Opportunity

Abbott Laboratories: Volatility Creates Opportunity

Overview

Abbott Laboratories has endured a difficult period in the stock market, with shares declining sharply through 2025 and into 2026. Yet, beneath the market noise, the underlying business continues to demonstrate many of the characteristics long-term investors seek: durable growth, strong cash generation, innovation-led expansion and a dividend record that places the company among the world’s leading healthcare franchises.

Q1 2026: A Business Still Delivering

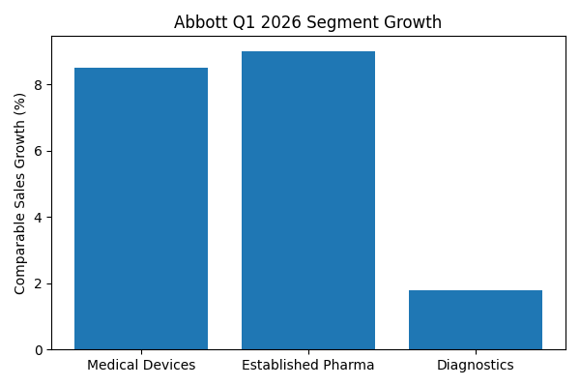

Abbott’s first-quarter 2026 results reinforced the resilience of the business. Adjusted diluted EPS reached $1.15, in line with company guidance and reflecting 6% growth. Revenue rose to $11.2 billion, driven by strong performance in Medical Devices and Established Pharmaceuticals.

Medical Devices remained Abbot’s standout division, with comparable sales growth of 8.5%, supported by double-digit expansion in Electrophysiology, Rhythm Management and Heart Failure. Diabetes Care also continues to benefit from the global adoption of the FreeStyle Libre platform, which remains as one of Abbott’s most significant growth drivers and a cornerstone of its long-term growth strategy.

Another key factor supporting Abbott’s investment case is diversification. Unlike many healthcare businesses that rely heavily on a single product category or patent cycle, Abbott operates across diagnostics, medical devices, nutrition and pharmaceuticals. That breadth allows weakness in one area to be offset by strength elsewhere, helping to smooth earnings and cash flow through different economic and healthcare cycles.

The company also benefits from significant geographic diversification. Established Pharmaceuticals continue to grow strongly across emerging markets, particularly in Latin America and Asia Pacific, where rising healthcare spending and expanding middle classes are creating long-term structural demand for affordable healthcare products.

The Exact Sciences Acquisition Could Be Transformational

The acquisition of Exact Sciences materially strengthens Abbott’s position in cancer diagnostics. Cologuard and Cancerguard provide exposure to one of the fastest-growing areas of global healthcare: early cancer screening and precision diagnostics. While the transaction is expected to create short-term EPS dilution of approximately $0.20 in 2026, the strategic rationale appears to be compelling.

Abbott’s international distribution footprint could significantly expand the reach of these products over time, particularly outside the United States where Exact Sciences previously had limited penetration. This gives Abbott an opportunity to scale proven diagnostic platforms across a much broader global market.

Just as importantly, Abbott’s innovation pipeline is not dependent on a single breakthrough product. The business has built a broad portfolio of technologies addressing multiple high-growth areas including cardiovascular care, diabetes management, structural heart procedures, and cancer diagnostics.

Why the Market Has Become Concerned

The recent weakness in Abbott’s share price appears to stem from three key concerns: temporary softness in the U.S. continuous glucose monitoring market, integration expenses related to the Exact Sciences transaction, and an FDA warning letter concerning testing and validation procedures at a FreeStyle Libre manufacturing facility.

However, none of these issues appear to undermine the long-term competitive positioning of Abbott’s core businesses. The FDA warning letter did not relate to patient safety or clinical effectiveness, while the long-term adoption opportunity for continuous glucose monitoring is still substantial.

The FreeStyle Libre platform remains particularly important in this context. Continuous glucose monitoring is still in the relatively early stages of adoption globally, and future reimbursement changes could materially expand the eligible patient population. Greater adoption among Type 2 diabetes patients not currently using insulin could represent one of the largest growth opportunities in healthcare over the next decade.

The Long-Term Growth Drivers Remain Intact

Against that backdrop, the broader growth story remains firmly in place. Abbott continues to invest heavily across Structural Heart, Diabetes Care, Electrophysiology and Cancer Diagnostics. The company currently has more than 200 clinical trials underway, alongside a broad innovation pipeline that is starting to move from development into commercialisation.

Early results from the VERITAS study for the investigational Amulet 360 device have been encouraging, while FreeStyle Libre 3 continues to demonstrate improved glucose outcomes in Type 2 diabetes patients. Abbott’s cardiovascular pipeline also continues to strengthen. Its next-generation Volt™ Pulsed Field Ablation system, approved by the FDA in December 2025 and now being rolled out, enables doctors to map, pace and ablate irregular heart rhythms using a single catheter.

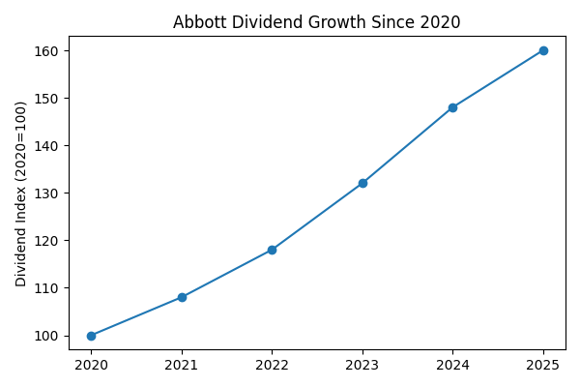

The dividend story remains equally compelling. Abbott has now paid 408 consecutive quarterly dividends and has increased its dividend for 54 consecutive years. Dividends have risen by more than 60% since 2020, supported by strong free cash flow generation.

Abbott’s financial strength adds strategic flexibility. The company maintains an AA- balance sheet rating from S&P and continues to generate substantial operating cash flow. This gives management capacity to continue investing in research and development, pursue selective acquisitions, support the dividend, and repurchase shares when valuations become attractive.

Conclusion

Markets often become overly focused on near-term disruptions, particularly when acquisitions or regulatory headlines create uncertainty. However, Abbott still appears to possess the core attributes of a high-quality compounder: global scale, diversified revenue streams, innovation leadership, resilient cash flows and a culture of returning capital to shareholders.

The current valuation appears to reflect a more pessimistic outlook than the operational performance suggests. For long-term investors willing to look through short-term volatility, Abbott may represent an increasingly attractive combination of quality, growth, and value.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as DGI, Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be shared or disseminated without our prior approval. This material has not been prepared for retail clients. Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’.

Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.