Semiconductors: the quiet industry powering the modern world

Semiconductors: the quiet industry powering the modern world

Overview

In 2025, the Financial Times’ Business Book of the Year was Stephen Witt’s The Thinking Machine, a story that helped bring Nvidia and the AI boom into the mainstream.

But, if there is one point we would emphasise for investors, it is this: the semiconductor industry encompasses much more than Nvidia.

Behind every AI model, every cloud data centre, every smartphone upgrade, and increasingly, every vehicle and factory, sits a global supply chain that is both astonishingly complex and surprisingly concentrated.

And that combination — complexity and concentration — is exactly why we continue to invest in the sector.

Why the semiconductor industry is attractive

Almost every major innovation of the past few decades, from personal computers and smartphones to electric vehicles, cloud computing and now AI, has relied on semiconductors.

Over the last 10 years, industry revenues have grown at roughly 9% per annum, reflecting a world that is becoming more connected, more digital, and more compute-intensive.

For investors, however, the most interesting part of the story is not simply growth.

The real story is barriers to entry

Semiconductors are unusual: innovation is relentless, yet competition at the highest level is extremely limited. That is because it is extraordinarily difficult to compete.

Building advanced manufacturing capacity is extremely expensive, technically demanding, and takes years to scale successfully.

At the leading edge, manufacturing tolerances are measured in atoms. Production happens in ultra-clean environments where even microscopic contamination can destroy yield. The complexity is so high that execution matters just as much as technology.

A concentrated industry structure has emerged

A simple way to understand the industry is to break it into three layers:

- Design houses (e.g., Apple, Nvidia, AMD) design chips

- Foundries manufacture them

- Equipment suppliers provide the critical tools used to make them

-

The design layer is highly competitive and fast-moving. But manufacturing and equipment have become increasingly concentrated. In many segments, one or two global companies dominate.

That structure has created a small number of world-class businesses that combine strong growth, high margins, excellent cash generation, and — importantly for our clients — the ability to grow dividends over time.

What has changed over the last decade

For decades, progress in semiconductor industry followed a relatively intuitive pattern: chips became smaller, faster and cheaper with each new generation.

That trend — often referred to as Moore’s Law — has slowed, but the demand for performance has not.

Complexity has accelerated — and so has cost

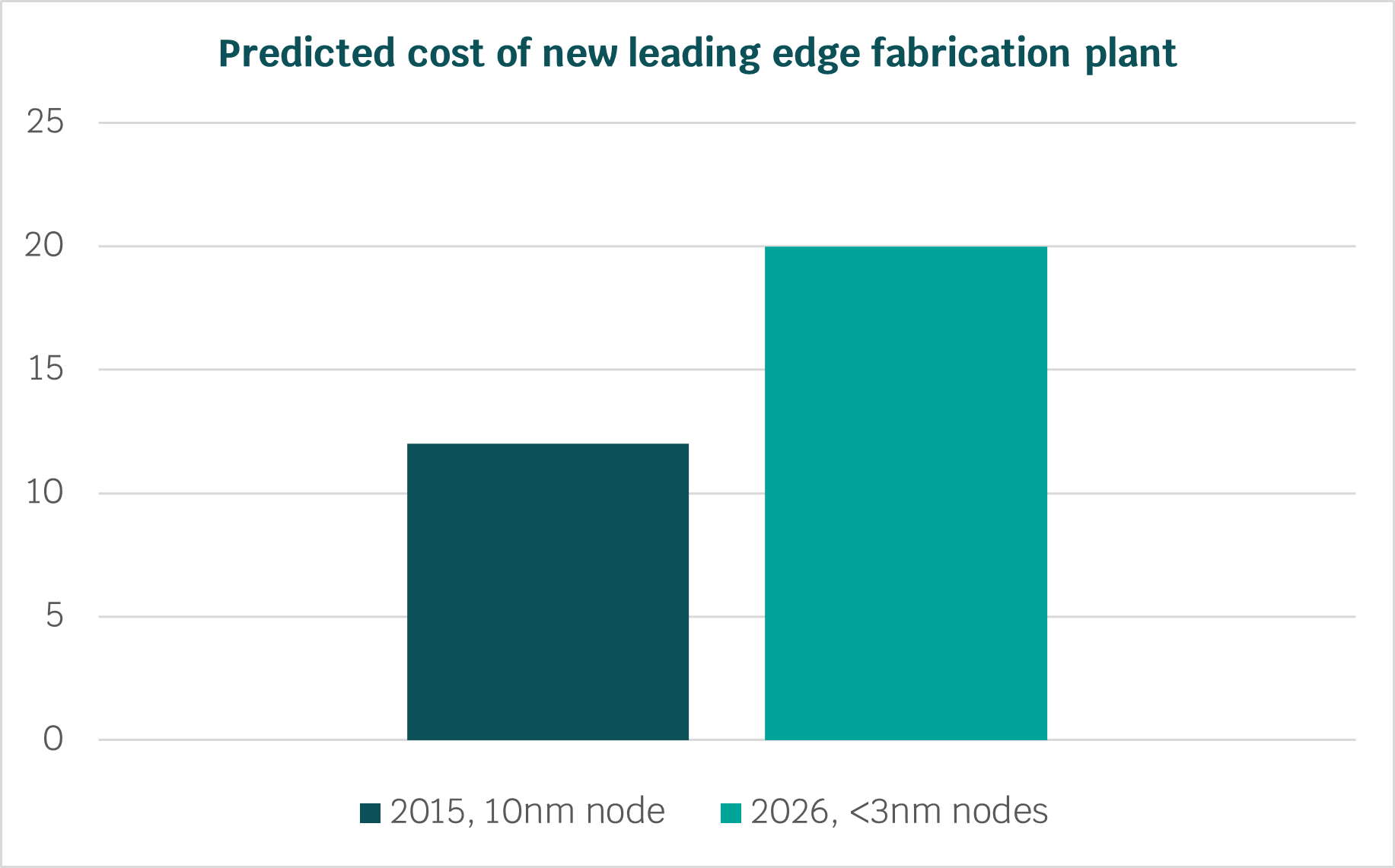

The cost of competing at the leading edge has risen sharply with each generation. For example, industry estimates suggested that a next generation ~10nm fab could require more than $12 billion of investment as far back as 2015. Today, a state-of-the-art <3nm facility is commonly discussed at well over $20 billion, depending on location and configuration.

And it is not just the buildings. Each new node requires more process steps, more precision, and a narrower set of specialist tools — reinforcing why the frontier is increasingly dominated by a small number of global leaders.

In other words, progress has become less about “shrinking transistors” and more about solving a growing set of engineering problems across manufacturing, materials, and packaging.

The investment implication: value has shifted

This matters for investors. When progress becomes harder, the companies with scale, execution capability, and the most specialised equipment tend to become more important, not less.

As a result, more of the value has moved toward the companies that manufacture chips and supply the critical equipment — not just those that design them.

While parts of semiconductors remain cyclical, the industry’s profit pool has increasingly shifted toward structurally advantaged bottlenecks — particularly leading-edge manufacturing and equipment.

CHART 1 - the rising cost of leading-edge manufacturing

As Moore’s Law slows, the cost of competing at the frontier has risen dramatically — reinforcing barriers to entry and industry concentration.

How we have positioned — and why we have owned these businesses for so long

Our semiconductor exposure is built around a simple idea: We invest in great businesses, and that includes semiconductor companies.

We do not try to compete as semiconductor physicists. Our edge is as generalist investors: identifying companies with durable competitive advantages, strong cash generation, and the ability to consistently compound shareholder returns over the long term.

That has led us to focus on the points in the value chain where market power is strongest — and where the industrial bottlenecks are most obvious.

TSMC: the manufacturing backbone of advanced compute

At the leading edge, TSMC is the company that repeatedly manufactures the most advanced chips in the world — at scale, at high yield, and with the reliability demanded by the world’s best designers.

TSMC’s competitive advantage is built on three pillars: scale, yield leadership and customer trust.

Over the long term, its record is striking in that manufacturing capacity has grown around 10% per annum over 20 years, and around 7% per annum over the last decade.

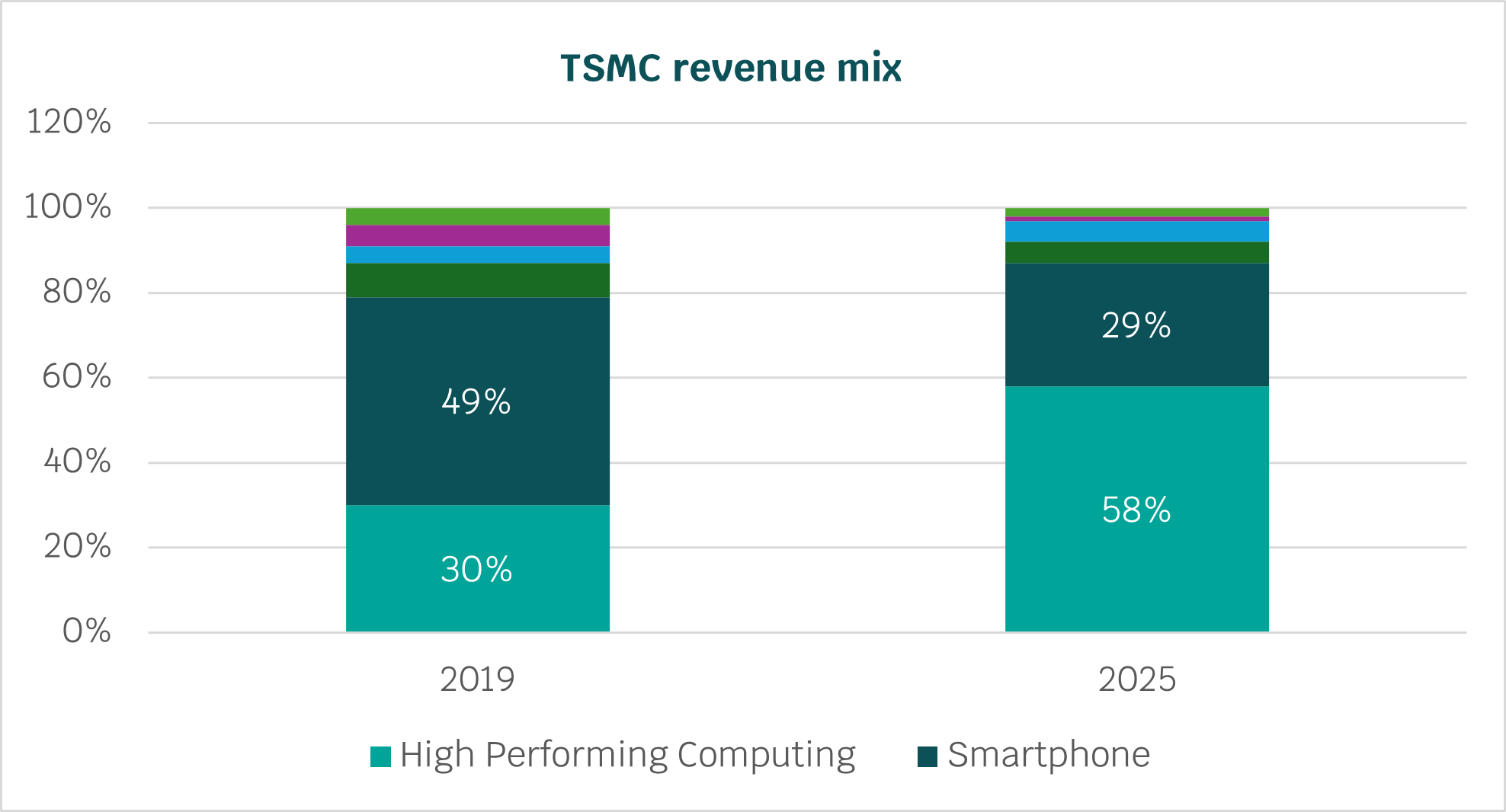

More importantly, its revenue mix has shifted meaningfully toward higher-value compute, with high-performance computing rising from 32% of sales in 2018 to 55% in 2025.

This reflects a shift toward more complex, higher-value chips — exactly where global investment is focused today.

TSMC has also consistently led major node transitions, from 7nm to 5nm to 3nm, reinforcing its strategic importance to the entire ecosystem.

CHART 2 - TSMC’s revenue mix has shifted toward higher-value compute

TSMC has become increasingly exposed to high-performance computing — a structural shift toward more complex, higher-value demand.

ASML: the heartbeat of the leading edge

If TSMC is the manufacturer, ASML is the toolmaker that makes leading-edge manufacturing possible.

ASML is the sole supplier of extreme ultraviolet (EUV) lithography machines — the most critical equipment required to produce the world’s most advanced chips.

Each EUV system costs several hundred million dollars, and the engineering complexity is extraordinary. ASML sits at the convergence of optics, lasers, materials science, precision engineering and systems integration.

There is no alternative supplier — and as chips become more complex, ASML’s monopoly position only strengthens.

That supports long-term growth, strong cash generation, and long-term dividend growth.

Why complexity matters

In many industries, complexity attracts competitors. In semiconductors, complexity has done the opposite — it has narrowed the field.

Disco: precision where it matters most

Disco is less well-known than TSMC or ASML, but it illustrates another part of our approach: investing in specialised industrial leaders in narrow niches.

Disco supplies grinding and dicing tools used in wafer finishing — steps that are becoming increasingly important as the industry shifts toward advanced packaging.

As Moore’s Law slows, progress increasingly comes from stacking chips, splitting chips into chiplets and integrating them through advanced packaging.

Technologies such as high-bandwidth memory are scaling rapidly, and packaging is becoming a bottleneck. Disco’s tools sit directly in that bottleneck.

Disco operates in narrow segments with limited competition, where precision and reliability matter more every year.

Where we are not invested — and why

It is worth being clear about what we are not trying to do.

We have not built our semiconductor exposure around the most visible headline designers. Those can be excellent businesses — but they often face more intense competition, faster product cycles, and greater valuation sensitivity to short-term expectations.

Similarly, we have tended to avoid more commodity-leaning segments of the market, where pricing power can weaken quickly when supply catches demand.

Instead, we prefer owning the enabling layers. These are the companies that multiple designers rely on, and where the barriers to entry are highest.

What we are watching next

One of the advantages of investing in manufacturing and tools is that it naturally leads you toward the frontier of industrial progress.

We are currently paying close attention to several themes shaping the next phase of semiconductor investment:

- High-bandwidth memory and the infrastructure required to feed AI accelerators

- Advanced packaging, as complexity increasingly shifts into assembly and integration

- Power semiconductors, including materials such as silicon carbide and gallium nitride

- The evolution of capex discipline across the ecosystem

These are areas where we expect the “industrial bottleneck” dynamic to persist.

Long-term perspective — with discipline

Semiconductors are often described as cyclical and in some parts of the market, they still are.

But for the dominant suppliers at the leading edge, the economics have become structurally more attractive:

- fewer competitors

- higher barriers to entry

- and a growing share of value accruing to manufacturing and tools

That said, we are very conscious of what we do not control.

AI-related capital spending is elevated and will fluctuate. Valuations across parts of the sector have rerated. And even leaders such as TSMC have increased capital commitments significantly in recent years.

This is precisely why we focus on businesses with market power, rising complexity, and capital discipline. Those characteristics underpin strong cash generation today — and, just as importantly for our clients, the ability to grow dividends sustainably over time.

In our view, semiconductors remain one of the most important long-term investment themes globally — but the best opportunities are often found not in the most famous names, but in the quiet industrial leaders that make the entire ecosystem work.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be share or disseminated without our prior approval. This material has not been prepared for retail clients.

Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.

In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.