The Twin Turbines of Dividend Growth

The Twin Turbines of Dividend Growth

Overview

One of the enduring privileges of investing on behalf of our clients is that it is as much a process of learning as it is of capital allocation — learning about how the world works, and, just as importantly, about the patterns in our own decision-making.

Recently, the investment team reviewed the outcomes of the stocks we have owned over the past decade, examining not only what drove our most successful investments, but also where others fell short. A clear conclusion emerged: over time, fundamentals mattered more than valuation. On average, the companies that delivered the strongest growth in revenues, profits and dividends also generated the best share price returns.

Just as importantly, our best investments improved as they scaled. Their returns on capital increased over time, reflecting businesses that required progressively less incremental capital to sustain growth.

The implication is straightforward albeit demanding. Our task is not simply to find growing companies, but to identify those where growth is accompanied by operating leverage, strengthening economics and rising capital efficiency — businesses where scale works increasingly in favour of shareholders rather than against them.

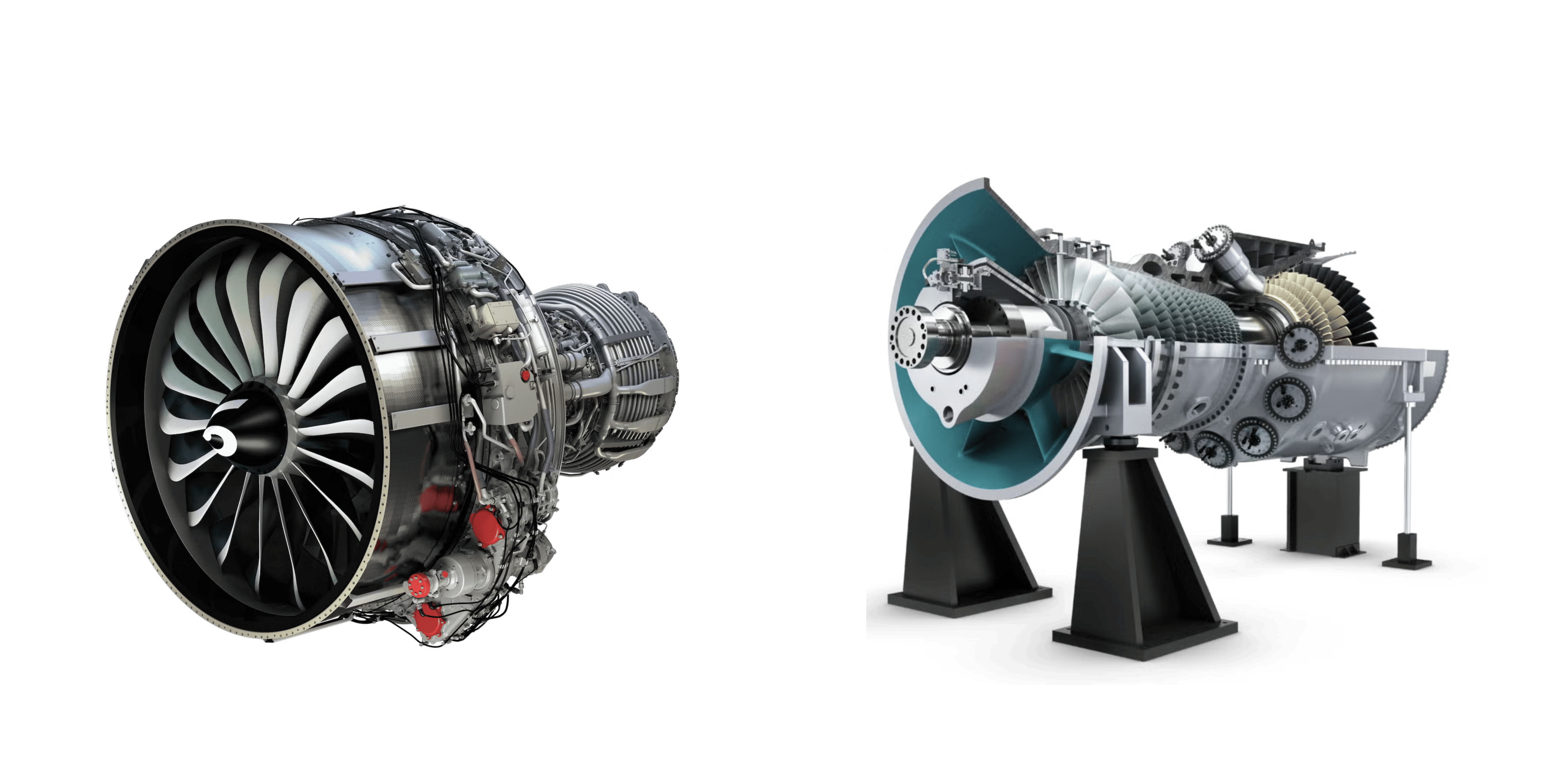

It is through this lens that we have added Safran and Siemens Energy to the portfolio over the past six months. Based in France, Safran designs, manufactures and services aircraft engines and aerospace systems whilst Germany’s Siemens Energy supplies gas turbines, grid infrastructure and long-term services to utilities, grid operators and industrial customers. Although they operate in different industries, both exhibit the characteristics we associate with our strongest long-term outcomes: visible revenue growth, improving margins, and the prospect of materially higher returns on invested capital over time.

The Ties That Bind

Both Safran and Siemens Energy occupy critical industrial bottlenecks, supplying complex turbine technology that are costly to design, difficult to replicate and deeply indispensable once installed. Whether enabling global air travel or underpinning modern power systems, these assets are mission critical, long lived and supported by recurring service revenues.

Both businesses are entering phases where revenue growth, margin expansion and improving returns on invested capital are beginning to converge. Large, visible backlogs provide multi year top line certainty, while rising utilisation and an increasing contribution from higher-margin aftermarket and service activity support operating leverage. As capital intensity eases and cash conversion strengthens, these dynamics should translate into growing distributable cash flow and the foundation for sustained dividend growth.

Safran represents the more mature expression of this model. Historically through its partnership with GE Aerospace, Safran helped develop the best-selling engine in aviation history, the CFM56. However, the partnership faced a huge technological challenge as it looked to develop the next generation LEAP (Leading Edge Aviation Propulsion) engine, a challenge that required the companies to overhaul their entire supply chain whilst maintaining production levels in the base business. The scale of that undertaking is difficult to overstate, as it took the better part of two decades to achieve.

Today, group returns on invested capital sit in the low to mid teens, reflecting a business that has already moved beyond the heavy investment phase of major engine programmes. As the LEAP engine programme matures and the earnings mix shifts further toward higher-margin spares and services, we see a credible pathway for returns on invested capital (ROIC) to continue rising over the next decade. That trajectory should be supported by pricing power, scale advantages and disciplined capital allocation. In that scenario, Safran would combine structural growth with returns comfortably above its cost of capital, strengthening its ability to compound cash flows and dividends across the cycle.

Siemens Energy is earlier in the journey, but the direction of travel is clear. Following several years of restructuring, reported returns on invested capital remain depressed by legacy losses and underutilisation. However, the balance sheet has been stabilised, loss making activities have been addressed, and record backlogs in Gas Services and Grid Technologies are beginning to convert into earnings. As margins normalise and service revenues scale, we believe ROIC can improve meaningfully, driven primarily by operating leverage rather than incremental capital intensity.

The Mechanics of Long-Term Dividend Growth

What links these two companies is not synchronised timing, but shared industrial logic. Both businesses benefit from long duration demand, high switching costs, significant barriers to entry and business models that increasingly favour higher-margin recurring service revenue over time. Just as importantly, both are positioned such that incremental revenue growth requires progressively less incremental capital, supporting stronger returns and improving cash generation as they scale. And both are transitioning into periods where returns on capital and free cash flow rise faster than revenues, creating the conditions for dividend growth that is sustainable rather than cosmetic.

Taken together, Safran and Siemens Energy illustrate the same investment proposition at different stages of maturity: industrially entrenched turbine businesses evolving into long term dividend compounders.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication, Dundas Partners LLP may be referred to as Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be share or disseminated without our prior approval. This material has not been prepared for retail clients. Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results.

document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.