Halma: Safeguarding Life, Driving Sustainable Growth

Halma: Safeguarding Life, Driving Sustainable Growth

Overview

Safety, health, and environmental technologies are powerful forces impacting society and shaping the future, and Halma is leading the way. Their focus on these vital themes has enabled them to build a portfolio of high-quality businesses that provide innovative solutions to some of the world’s most pressing challenges, making everyday life safer, cleaner, and healthier for millions of people.

As regulation tightens and sustainability becomes a strategic imperative, these solutions move from “nice to have” to non-negotiable. That shift gives companies like Halma structural growth visibility for decades to come.

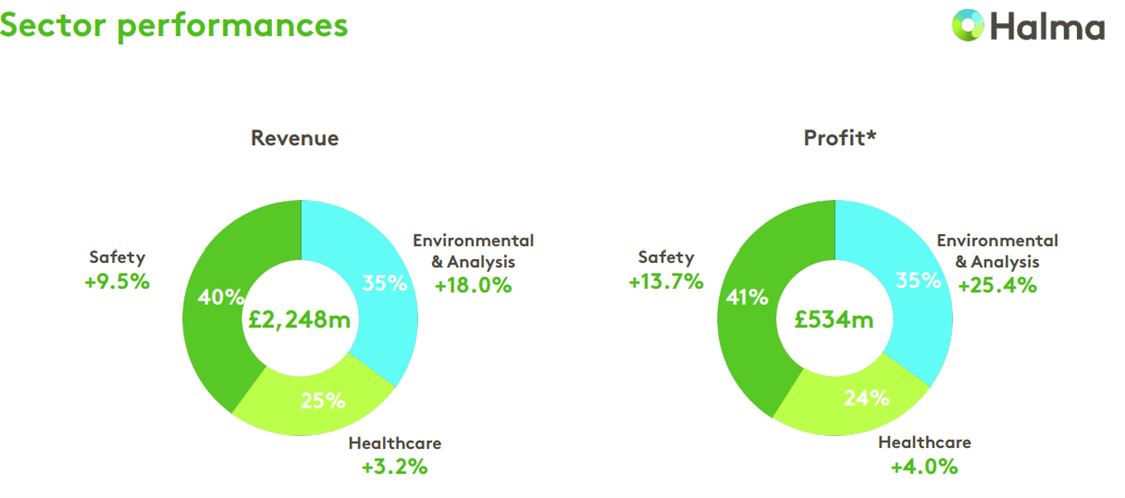

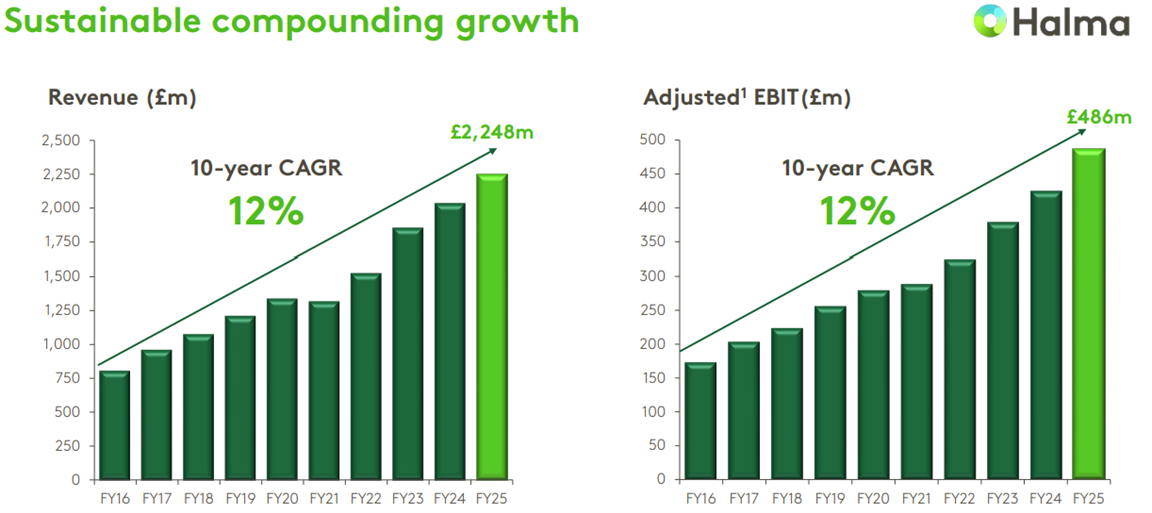

With roots stretching back to 1894, and a place in the FTSE 100, Halma has grown into a global group with over 45 specialist businesses, operating in 20 countries and generating annual revenues that exceed £2 billion.

The Secret to Enduring Growth

Halma combines decentralised entrepreneurship with central discipline. Each subsidiary operates as a focused, agile business led by entrepreneurs who know their customers and markets intimately. They have the freedom to innovate, invest and expand, but within a tightly defined financial framework that enforces accountability and return on capital discipline.

This model delivers the best of both worlds: small-company agility with big-company stability. It attracts exceptional leaders who stay and build over the long term, compounding value through innovation and operational excellence. Continuous reinvestment in R&D, coupled with a relentless focus on high-margin, high-return niches, allows Halma to generate enduring high growth — growth that is durable, repeatable, and capital-light.

The Catalysts of Growth

Sprawling industrial conglomerates and diversified roll-ups often give investors reason for caution. Burdened by their own complexity, leveraged acquisitions, and lack of focus, they can struggle to deliver favorable shareholder returns. We believe Halma is one of the very few that are the antithesis of this model. Their sector focus tilts their portfolio to growth markets, underwritten by regulation, protected through high barriers to competition, and the needs, not wants of a diversified customer base.

Halma does not buy distressed businesses but rather opts for high-quality niche businesses with defensible market positions. Most deals are funded through operating cash flows, keeping debt levels low and financial flexibility high.

The Group’s proven “buy and build” strategy emphasises continual reinvestment at the business unit level, but with strict capital allocation guidelines. Each business is expected to continue to thrive under Halma ownership, with no interest in running them for cash. And, if they do not, they are divested.

The company’s decentralised model empowers entrepreneurial leaders within each subsidiary, fostering innovation, agility and accountability. The whole business is aligned around a clear growth algorithm for mid-single digit organic growth, plus mid-single digit growth through acquisitions, with incremental margin improvements supporting low-double digits earnings growth. This balance of autonomy and discipline ensures that Halma’s growth remains both consistent and value-accretive for shareholders.

Financial Highlights and Diversification

Halma’s competitive edge lies in its disciplined acquisition strategy, robust R&D investment, and ability to scale specialist businesses globally giving shareholders the potential for “right tail” outcomes. A prime example is Avo Photonics, purchased in 2011 for $20m, which at the time generated $5m in sales. Since then, the business has become central to AI data center capital expenditure, developing products and services essential to low latency data transfer. As of 2025, photonics now generates $500m in annual sales, around 15% of group sales and 50% of organic growth. Halma is now operationally leveraged to hyperscale capital expenditure seeing the AI revolution. Due to this success, Halma now has embedded optionality: they can reinvest the proceeds of this rapid growth in a disciplined manner, or they can dispose of this asset. Either way, shareholders will be handsomely rewarded through their foresight.

In 2025, Halma reported revenues of over £2.2 billion, with organic revenue growth in the high single digits, operating margins rising above to above 20%, with profits rising 15% as a result. The company’s progressive dividend policy has seen payouts rise for over 46 consecutive years, a testament to its resilience and consistent cash generation.

Why We Still Hold – Enduring, & Long-Term Tailwinds

Halma continues to benefit from powerful long-term drivers: tightening safety standards, demographic shifts in healthcare, and accelerating demand for environmental technologies. Its decentralised model and disciplined reinvestment have delivered outstanding returns through every market cycle.

We first bought Halma in October 2023, for under £19 per share, having waited for an opportunistic entry point since 2020. Since then, the shares have rallied strongly to over £35 per share, now trading on a premium valuation at 28x cash flow. Halma’s track record of compounding earnings growth should improve due to the outlook for above trend organic growth with margin expansion.

Management’s disciplined capital allocation, commitment to growing dividends, and resilience through economic cycles make Halma a core holding for long-term investors.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as DGI, Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be share or disseminated without our prior approval. This material has not been prepared for retail clients.

Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.

In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.