Leading the Pack: Zoetis and the Future of Animal Health

Leading the Pack: Zoetis and the Future of Animal Health

Overview

When investors consider pharmaceuticals, the spotlight usually falls on human medicine, with its complexity and volatility. Yet in the background, animal health has emerged as an enduring and compelling growth story. Zoetis sits at the forefront of this trend: a global leader using innovation to redefine how we care for animals worldwide.

Zoetis, originally founded within Pfizer in 1952 and spun out in 2013,has grown into the world’s largest and most trusted animal health company. Withmore than $9.3 billion in annual revenue, operations in over 45 countries, anda market cap around $65 billion, Zoetis is not merely expanding, it is leadingthe pack and setting the standard in animal health.

The Catalyst for Growth

We first reviewed Zoetis upon its demerger from Pfizer in 2013. History tells us that buying a newly independent company can be attractive because, once separated from a larger corporate parent, it often gains sharper strategic focus, stronger management accountability, and operational efficiencies that were previously lost within the broader organisation’s priorities. This was certainly the case here.

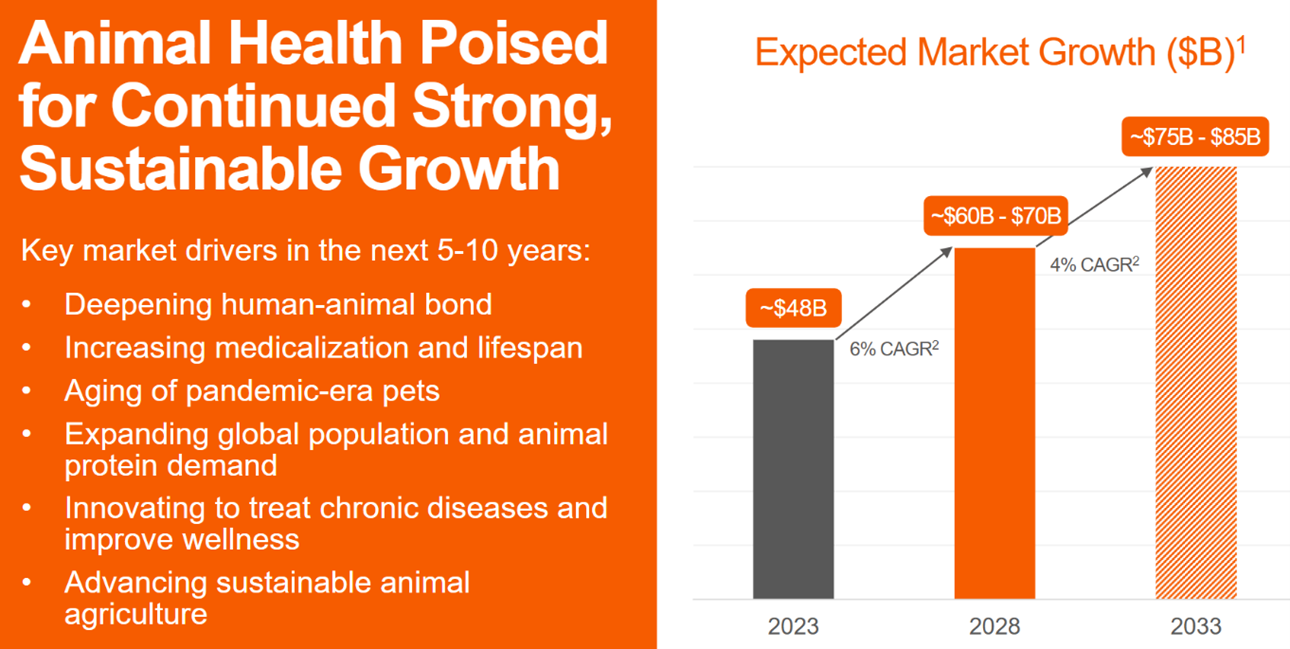

We also understood that Zoetis sat at the intersection of three powerful growth drivers: the increasing ownership and humanisation of pets, advances in veterinary medicine and growing global demand for efficient livestock production.

We placed Zoetis in context by comparing it with global peers such as Elanco and Merck Animal Health in the U.S. and Virbac in Europe. The lesson was clear: scale and diversification matter and create enduring advantages. Zoetis spreads R&D across a broad portfolio, focused on first to market products where they can gain high market share and premium pricing. Unlike rivals, which either face balance sheet constraints or lack the global reach to compete effectively, Zoetis combines high quality, internal manufacturing, allowing them to reap the benefits of economies of scale as products ramp up, while also retaining the ability to adapt rapidly to changing market dynamics.

Our deeper dive revealed Zoetis’ ability to diversify revenues through multiple segments:

- Companion animal products, particularly dermatologytreatments like Apoquel and Cytopoint, have delivered strong double-digitgrowth as pet owners increasingly treat chronic conditions.

- Livestock solutions in vaccines and anti-infectives provideresilience, supporting global protein production even in cyclical downturns.

- And, a growing portfolio of diagnostics and digital tools, whichadds another layer of growth and helps veterinarians make faster, more accuratedecisions—extending margins and deepening loyalty.

Moreover, in FY2024, Zoetis posted revenues of $9.3 billion, up 8% despite currency headwinds, with companion animal growth of 13% and livestock steady. Operating profit grew 11%, while free cash flow supported continued reinvestment and a 15% increase in dividend.

Why We Still Hold – Clear Value & Long-Term Tailwinds

Given the structural and strategic tailwinds of pet ownership, global protein demand, and veterinary care innovation, we believe Zoetis can scale well beyond today’s size. Its combination of high-margin growth and diversification should lead to significant dividend growth and share price appreciation for long-term investors.

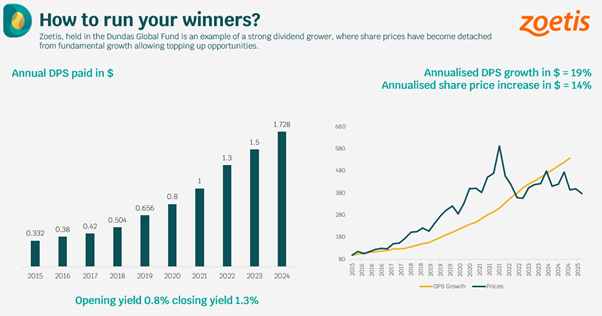

Despite the shares compounding at 14% per annum and the companyincreasing its dividend at 19% per annum, Zoetis shares have underperformedsince the end of COVID. They currently trade on 22x next year’s earnings, yield1.5% which is a discount to both history and its valuation relative to the MSCIACWI index.

In our view, the market is undervaluing the durability and breadth of itsgrowth. Zoetis is not just a beneficiary of long-term trends—it’s helping shapethem.

In an increasingly crowded investment universe, Zoetis remains a rarebreed.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as DGI, Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be share or disseminated without our prior approval. This material has not been prepared for retail clients.

Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.

In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.